TODAY’S MORTGAGE RATES Mortgage Rates went up about .08% on the week with the Mortgage…

No More 100+ Calls When You Apply for a Mortgage 🙌

TODAY’S MORTGAGE RATES

Mortgage Interest Rates moved up slightly

with the Mortgage Backed Security (MBS)

Market trading down – 8 bps over the past

7 days. Despite the small increase, interest

rates are still sitting very close to their

lowest levels of 2025.

Below are your average interest rates

across the country according to

Mortgage News Daily.

Last week was a relatively slow data

week for interest rate movement.

The big news is the makeup of the

FED and potential future movements.

One FED reserve member, Adriana

Kugler, resigned effective 8/8/2025.

This gives President Trump the ability

to nominate a new member that will

theoretically side with his views on

future FED actions. On Thursday,

President Trump selected Stephen

Miran to replace Adriana Kugler.

Jerome Powell’s term as FED Chief

goes until May 2026. It’s no secret

that President Trump has been unhappy

with the FED not lowering the Federal

Funds Rate. Now the question goes

to who will replace FED Chief Powell

and how will they manage monetary

policy.

FED member Michelle Bowman stated over

the weekend that she thought the FED

should lower rates 3 times through the

rest of the year by 75 bps due to

concerns within the labor market. It

appears that we may be on the way

to the FED lowering the FED funds rate

more aggressively in 2025 or 2026.

Remember that the Federal Funds Rate

does not directly impact mortgage interest

rates, but the FED rate definitely has an

impact on the economy and mortgage rates.

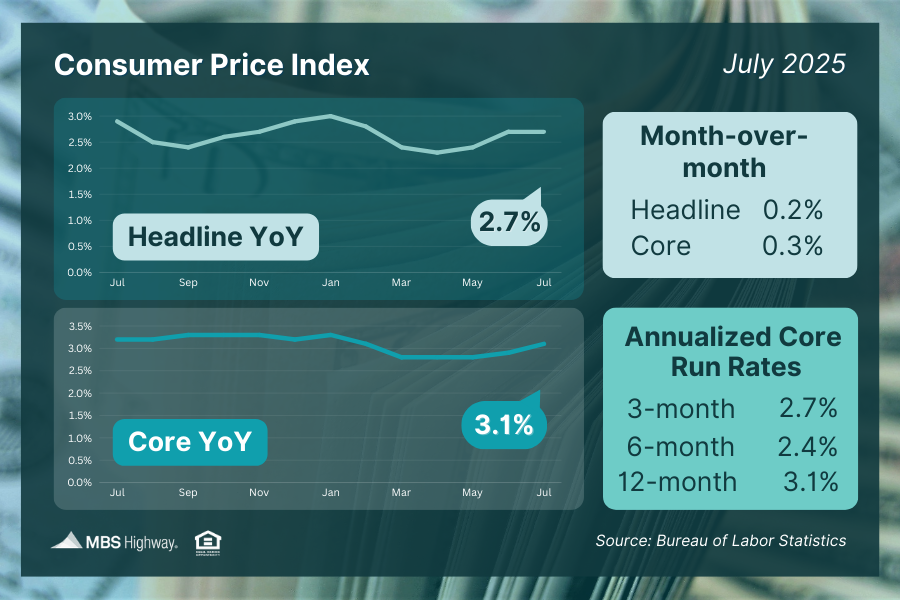

This week the big potential market movers

are the CPI and PPI inflation reports. The

CPI inflation report was released just

before this writing.

CPI Year over Year Inflation decreased

to 2.7%. Core CPI inflation increased

to 3.1%. Both numbers were close to

expectations.

There are a lot of characteristics

that go into a mortgage rate –

credit score, investor, loan to

value, loan amount, costs, etc.

Please call me to go over your specific

scenario so we can price your loan

out accurately.

Or you can get a Free Mortgage Quote

or Apply for a Mortgage with the links below.

Thank You!

OR

Thank you!

TRIGGER LEAD BILL PASSES

Most Mortgage Professionals are rejoicing

at the passage of a bill that will ban credit

companies from selling mortgage credit

inquiry information to most mortgage

companies.

When a consumer does a hard pull

on their credit for a mortgage, the

credit bureaus sell that information to

other mortgage companies to solicit

the customer. With mortgage volume

down over the past few years, there are

more companies purchasing these leads.

The effect has been a consumer getting

100’s of calls and illegal texts soliciting

them. Imagine trying to work and getting

100’s of calls and texts that you didn’t

ask for and weren’t expecting.

This is a positive for consumers and

the mortgage industry as these trigger

companies have become more and more

invasive in the amount of calls, texts

(which require a text opt in they never

have), and even going as far as

imitating the mortgage company that

pulled the original consumer credit.

Mortgage Credit inquiries can still

be sold to:

1. The entity that originated the consumer’s

current residential mortgage (if applicable)

2. The entity that services the consumer’s

current residential mortgage (if applicable)

3. A depositary institution or credit union

that holds a current account for the

consumer.

Number 3 is a prime example of the bank

industry’s lobbying power in Congress.

President Trump has not signed the bill

yet. Assuming he does sign the bill,

rules banning the sale of selling

mortgage credit inquiries to most

mortgage companies will go into effect

in 6 months.

Hope you have a fantastic week!!