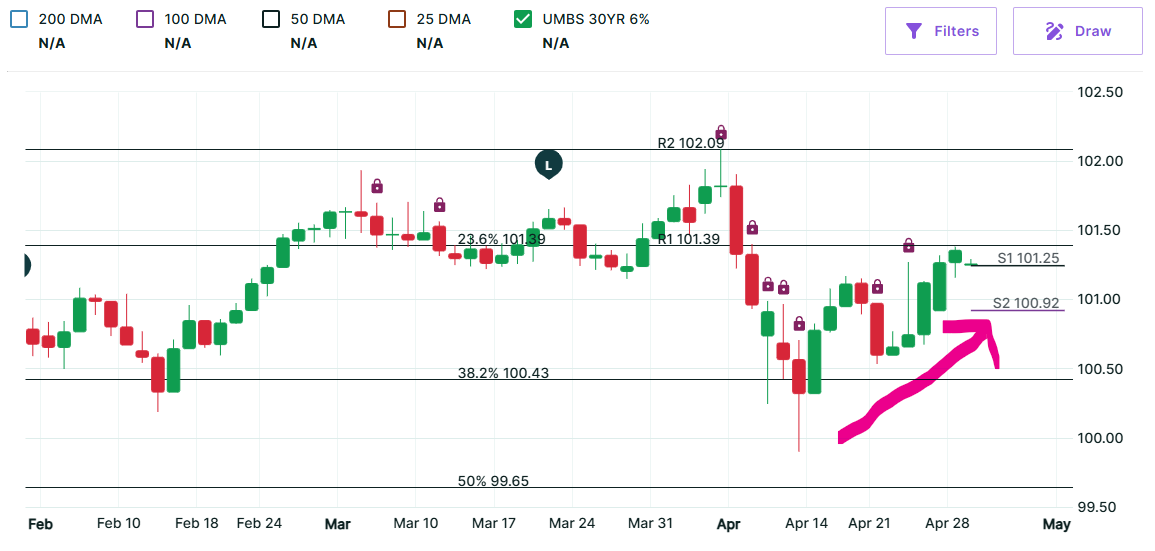

TODAY’S MORTGAGE RATES Mortgage Rates improved about .05% on the week with the Mortgage Backed…

🚨 Market Shifts – 0.2% Rate Dip Ahead of Big Economic News

VIDEO UPDATE:

Great Week for Interest Rates, Here is Your Weekly Mortgage Rate Update!

TODAY’S MORTGAGE RATES

Mortgage Interest Rates have had a

really good week with the Mortgage

Backed Security (MBS) Market

trading up + 91 bps.

Interest Rates fell approximately

.2% over the past 7 days.

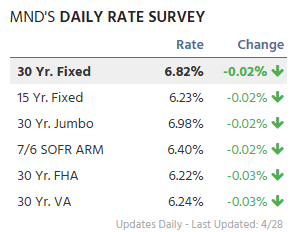

Below are your average interest rates

across the country according to

Mortgage News Daily.

Economic data was slow last week

but we have a big week ahead of

us this week. Then the following

week we have the FED Meeting.

First, we have U.S. GDP for

Quarter 1. This should give us a

good idea of the current status of

economic growth in the U.S. Many

experts are expecting little to no

growth which is usually positive

for interest rates.

The PCE inflation report comes out

Wednesday and most expectations

are for the monthly inflation number

to be low. This would normally help

interest rates but since these figures

are before Tariffs, it may not cause

much market movement.

Lastly, we have Friday’s April BLS

Jobs Report. Lower job creation and

higher unemployment typically help

interest rates. Higher job creation and

lower unemployment typically hurt

interest rates.

There are a lot of characteristics that

go into a mortgage rate – credit score,

investor, loan to value, loan amount,

costs, etc. Please call me to go over

your specific scenario so we can

price your loan out accurately.

Or you can get a Free Mortgage Quote

or Apply for a Mortgage with the links below.

Thank you!

or

JUMBO 40 YEAR INTERST

ONLY MORTGAGE

Jumbo Payment Smart is a Mortgage

Product that helps clients with loan

amounts over the conventional limit

get maximum flexibility with their

mortgage payment. Here is how

the product works.

For the first 10 years, the loan is

Interest Only. This gives a client the

ability to have a low monthly payment,

but also a lot of flexibility to pay

down the loan and lower their

payment further.

Unlike a traditional mortgage

amortization where interest is

preloaded at the beginning of the

loan, an interest only loan has

no money going towards principal.

Anything the client pays over the

minimum monthly payment will

go directly towards principal.

Because the monthly payment is

calculated off the principal balance,

every time the client pays down the

loan, they lower their required

monthly payment.

After the initial 10 years, the loan

turns into a 30-year fixed amortization

where the client is required to pay down

principal like a normal 30-year

fixed mortgage.

When used correctly, this product gives

clients a lot of flexibility to pay down

their mortgage on some months,

while keeping more funds in their

pocket on other months.

Contact me if you would like to

discuss how this product could work

for you.

MORE HOUSING OPTIONS FOR

YOUR NEXT MOVE

Housing inventory has increased nationally

to about a 4-month supply as of April 2025.

As more sellers put their home on the

market, it gives clients more options

and more negotiating power in terms

of price and seller concessions.

Although housing inventory is higher

relative to the past 5 years, inventory

is lower than it was before the

pandemic.

Hope you have a fantastic week!