TODAY’S MORTGAGE RATES Mortgage Rates improved close to .1% on the week with the Mortgage…

Why Mortgage Rates Just Jumped (and Where They’re Headed)

TODAY’S MORTGAGE RATES

Mortgage Rates went up .2% on

the week with the Mortgage Backed

Security Marketing Trading down -81

bps.

Here are your Average Mortgage

Rates across the country according

to Mortgage News Daily.

A 30 Year Fixed Conventional Rate at

6.68% – equates to a $643.95 Principal

and Interest Payment per $100,000 in

Loan Amount. If you would like me to put

together scenarios for your situation, feel

free to contact me or use my Free

Mortgage Calculator below:

Mortgage Calculator – Green Home Loans

The main component that continues to

impact interest rates:

Higher Oil Prices – Oil prices are

currently over $100 / Barrel

Uncertainty on the situation in

the Middle East

Both situations are impacting inflation.

We had 2 inflation reports released

last week – The Consumer Price

Index and the Producer Price Index.

On Friday, Kevin Warsh will be sworn

in as Chair of the FED. Kevin Warsh

has the difficult agenda of trying to

bring down borrowing rates for

consumers while keeping inflation

in check.

Most experts do not believe the FED

will cut the Federal Funds rate

through the rest of 2026.

There are a lot of characteristics

that go into a mortgage rate –

credit score, investor, loan to

value, loan amount, costs, etc.

Please call me to go over your specific

scenario so we can price your loan

out accurately.

Or you can get a Free Mortgage Quote

or Apply for a Mortgage with the links below.

Thank You!

OR

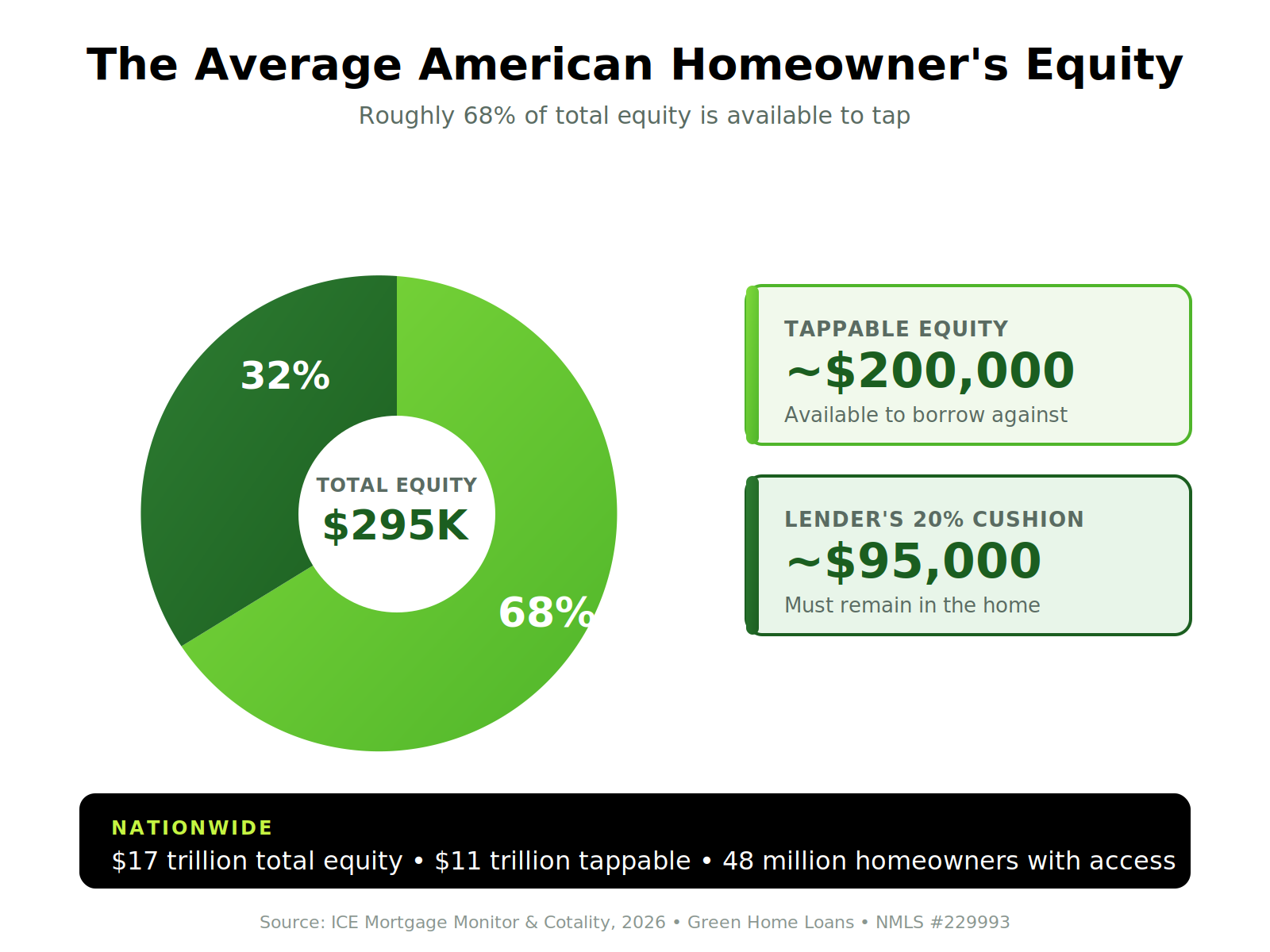

PUT YOUR HOME EQUITY TO WORK

If you’re carrying high-interest credit

card or consumer debt, the solution

may be sitting right above your head.

American homeowners are holding a

record $17 trillion in equity, with the

average mortgage-holding homeowner

sitting on roughly $200,000 in tappable

equity. That’s real borrowing power – and

right now, the math is hard to ignore:

• Credit cards: ~22% APR

• Personal loans: ~13% APR

• HELOCs: ~7–8% APR

Carrying $50,000 on credit cards at

22% costs about $11,000 a year in

interest. That same balance to a HELOC

at 8%, and you’re paying around

$4,000 – a savings of $7,000 a year.

A HELOC lets you tap your equity

without touching your existing mortgage,

so if you locked in a low rate during the

pandemic, it stays put. You only pay

interest on what you use, and the

interest may even be tax-deductible

when used for home improvements

(check with your tax advisor).

If you’ve got equity and high-interest

balances, let’s run the numbers

together. A quick conversation could

save you thousands.

I hope you have a fantastic week!!