Instagram TODAY’S MORTGAGE RATES Mortgage Rates went up .2% on the week with the Mortgage…

🏡 Fixed or Adjustable — Which One Actually Saves You More?

TODAY’S MORTGAGE RATES

Mortgage Rates saw some nice improvement

with the Mortgage Backed Security (MBS)

market trading up +21 bps on the week.

Here are your Average Mortgage Rates

across the country according to

Mortgage News Daily.

With not much data being reported,

all eyes are on the FED.

FED Chair Powell spoke on October

14th and he stated that the FED may

stop the runoff of Bonds and Mortgage

Backed Securities on their

balance sheets.

Here is what this means in layman’s

terms:

The FED is currently allowing up to

35 billion in Mortgage Backed Securities

and 5 billion in U.S. Treasuries to mature

and not reinvest those funds back into

more Bonds and Treasuries. If they

limit this run off, they would essentially

be investing more money back into U.S.

Treasuries and Mortgage Backed

Securities which should help interest

rates.

The FED is also meeting with a statement

and press conference on 10/29/25.

According to experts, there is close to

a 100% chance of another Federal

Funds Rate Cut. The market is already

expecting the rate cut and it is

currently built into rate pricing.

The FEDs comments about future moves

will likely dictate how rates react to the

FED decision.

COULD AN ARM BE A

BETTER OPTION?

Adjustable Rate Mortgages are typically

fixed for 5, 7, or 10 years. ARMs have

become increasingly popular because

they typically offer a better payment

and rate than a fixed mortgage.

We are usually seeing 5/6 ARMS –

fixed for 5 years and adjusting every

6 months afterwards, pricing about

.375% better than a 30-year fixed

loan with the same costs.

And 7/6 ARMs – fixed for 7 years and

adjusting every 6 months afterwards,

pricing about .25% better than a 30-year

fixed loan with the same costs.

With ARM loans, you are usually

going to pay a point to a portion of

a point, because the rate savings

aren’t as substantial on a 0-point loan.

ARM loans typically save a customer

more money even if they stay in the

loan after the fixed period, based

on historical averages of adjustable

interest rate movements.

An ARM loan is not the best product

for every customer, but an ARM could

be a great option if you plan on not

being in your loan over the fixed

period of time, or you have a bit

higher of a risk tolerance.

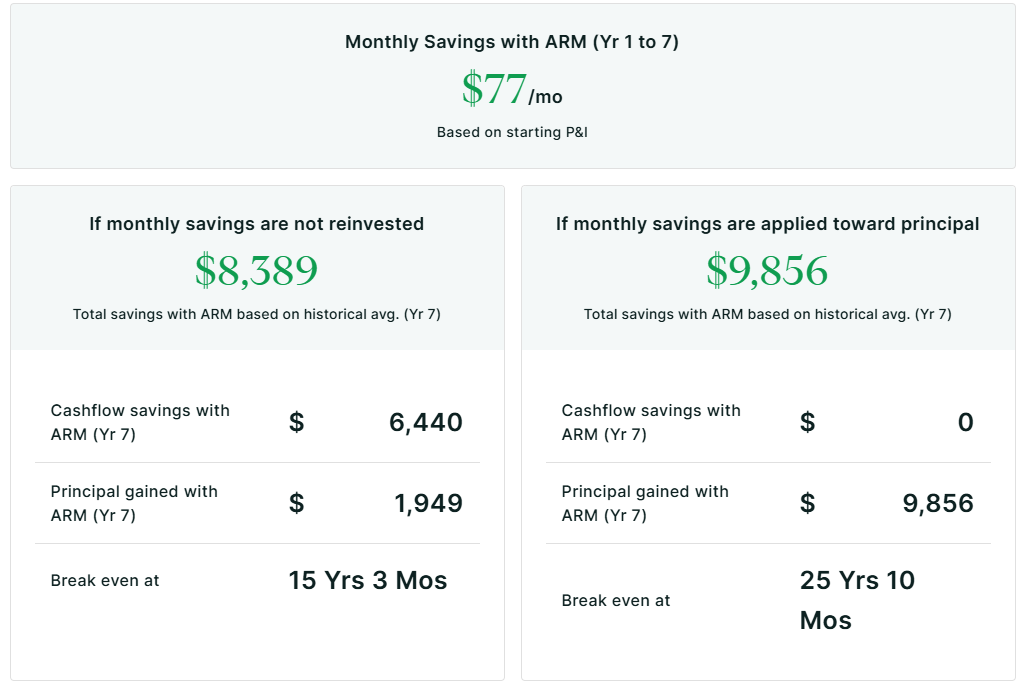

Here is how much you would save

comparing a 30-year fixed mortgage and

a 7/6 ARM on a $500,000 loan. This

comparison assumes that interest rates

will adjust after the fixed period based

on historical averages.

On the 7/6 ARM, if you kept monthly

payment savings in hand, you would

save more money with an ARM until

15 years and 3 months, a full 8+ years

after the loan adjusts.

Your principal balance on a 7/6 ARM

would be lower for over 7 years.

Hope you have a fantastic week!!